The Board of Directors of IVS Group S.A. (Milan: IVS.MI), convened on September 7th, 2023, and chaired by Mr. Paolo Covre, examined and approved the Half-Year Financial Report at 30 June 2023, as summarised below.

Summary of results at 30 June 2023

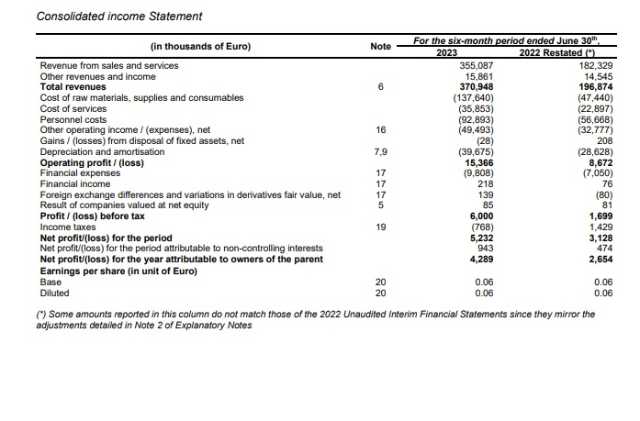

- Consolidated revenues: euro 370.9 million, +88.4%, compared to June 2022.

- Ebitda: euro 55.0 million. Ebitda Adjusted: euro 57.4 million, +54.9%.

- Ebit: euro 15.4 million, +77.2%. Ebit Adjusted euro 17.7 million (+110.6%).

- Consolidated Net Profit: euro 5.2 million. Net Profit Adjusted: euro 7.1 million (+128.4%).

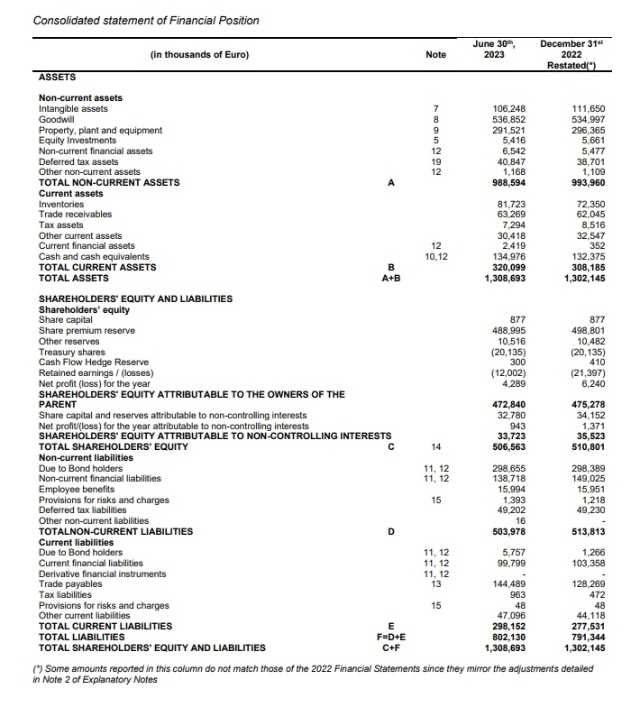

- Net Financial Debt equal to euro 402.8 million, (including Euro 64.0 million debt related to IFRS 16 and euro 10 millioni dividend) from Euro 417.0 million (restated) at the end of 2022.

Operating performances

Consolidated revenues in 1st Half 2023 reached euro 370.9 million, +88.4% compared to euro 196.9 million in 1st Half 2022, that did not include the businesses entered in IVS Group since July 2022 after the business combination with GeSA and Liomatic.

According to the new division of the groups’ activities, the operating businesses showed the following turnover performances (before intra group elisions).

- Vending business (including four areas: Italy, France, Spain and other countries): euro 6 million, +52.0% compared to 185.2 million at 30 June 2022, further divided into the following markets: (i) Italy (euro 235.8 million, +55.1%), (ii) France (euro 24.3 million, +23.0%), Spain (euro 8 million, +29.1%), (iv) other Europe markets (euro 5.9 million, +339.0%). Italy includes most of Liomatic vending businesses and GeSA; France has the same previous IVS Group perimeter; Spain includes also some local Liomatic vending business; the other European markets include the former IVS Group businesses in Switzerland and Poland, and those of Liomatic in Germany, Portugal and San Marino.

- Resale business: euro 1 million not present before the business combination and therefore the comparison between 2023 and 2022 is not significant. Through the acquired businesses, the group is now the Italian market leader also in this important market segment.

- horeca business: euro 11.6 million. This is also a new business segment for IVS Group, and it is mostly represented by activities owned by Liomatic (in Spain), and some business started by IVS in the second half of 2022.

- Coin division business: euro 18.2 million (+44.9%), with no contributions from the business combination, but including N-and Group, specialized in production and sale of touch screens, mostly destined in the vending sector, and in the improvement of digital users’ interfaces), showing a sales growth in all the most important businesses, and the ongoing increase of the payment app CoffeecApp (over 1.38 million registered users and around 367,000 active users).

The total number of vends at June 2023 was equal to 515.5 million +49.5% from 344.7 of Ivs Group only at June 2022 before the business combination.

Average price per vend (net of VAT) was equal to euro 51.40 cents, from 50.10 cents (+2.6%) of IVS Group in the same period of 2022 (before thebusiness combination). The actual price increase in percentage was higher, but the new average includes the selling prices of Liomatic and GeS that, compared to IVS, in the Italian market are quite similar for Liomatic (that however has a higher cost of goods sold) and are around 10% lower for GeSA.

The price increase policy will continue to deploy its effects for quite a long time on the whole client’s base.

In homogeneous terms, as if the business combination were already completed at the beginning of 2022, would emerge an increase of sales of 10.8%, and 14.8% of Adjusted Ebitda; this confirm the first positive effects deriving from the integration.

Ebitda is equal to euro 55.0 million, increased by 47.6% compared to euro 37.3 million at June 2022. Ebitda Adjusted is equal to euro 57.4 million, +54.9% from euro 37.0 million at June 2022. The margins of the business areas, with their different levels of profitability, in particular between vending and resale business, start to reflect the positive effects expected from the business combination.

Ebit Adjusted increased by 110.6% to euro 17.7 million, from euro 8.4 million at June 2022, thanks to the Ebitda growth and despite the growth of depreciation charges, that mostly reflect the allocation to amortisable assets of some parts of the purchase price and goodwill emerging from the business combination (around euro 3.5 million of higher depreciation in the first half of the year).

Pre-tax Profits at June 2023 strongly increase to euro 6.0 million, from euro 1.7 million of 2022.

Consolidated Net Profit at June 2022 is equal to euro 5.2 million (with euro 0.9 million net profit attributable to minorities) compared to euro 3.1 million of 2022 (that included euro 1.4 million pf positive tax proceeds). The Net Profit Adjusted for the exceptional items is equal to euro 7.1 million, from euro 3.1 million at June 2022 (with euro 1.0 million minorities).

Net Financial Position (“NFP”), is equal to euro -402.8 million (including Euro 64.0 million debt deriving from rent and leasing contracts according to the definitions of IFRS 16), decreased by euro 14.1 million from euro -417.0 million (restated), of which Euro 69.4 million of IFRS16 effects, at the end of 2022. In the Net Debt are included euro 10.0 million dividend (approved in June by the AGM and paid in July) and euro 6.3 million interests accrued on the bind expiring on October 2026, while is not included the VAT credit (Euro 11.6 million at the end of June 2023).

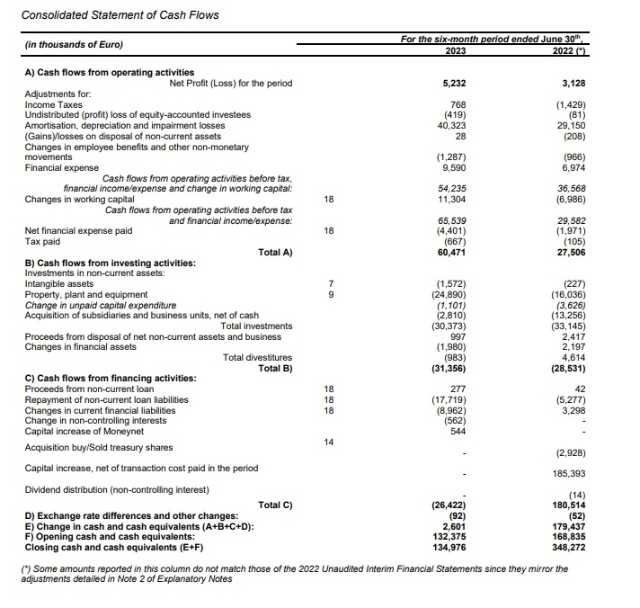

During the 1st Half 2023 the group generated an operating cash-flow of euro 60.5 million (euro 27.5 million in the 1st Half 2022). Payments for net Capex were equal to euro 26.6 million (euro 17.5 million in the 1st Half 2022) and euro 2.8 million for M&A (euro 13.3 million in 1st Half 2022).

Other significant events occurred after 30 June 2023 and prospects for the year

2023 will represent for IVS Group the first full year with the new activities and organisation arising from the business combination, effective on July 2022. The integration, aimed at obtaining cost and revenues synergies, is proceeding according to plans, with a complete achievement of the expected benefits in a period of around two years from the transaction.

The present scenario, with a high inflation and the consequent impact on consumptions, slowed-down the full recovery of sales volumes to the levels before Covid expected at the beginning of 2022, but it makes even more valuable the significant possibilities of improvements within the group, thanks to its larger size.

In the core vending business it is expected the important symbolic target of 1 billion vends at the end of 2023, with an increase of the margins in all the business areas.

IVS Group results